Key Benefits Setting Paramount Term Life Plans Apart

Robust coverage with no medical exams

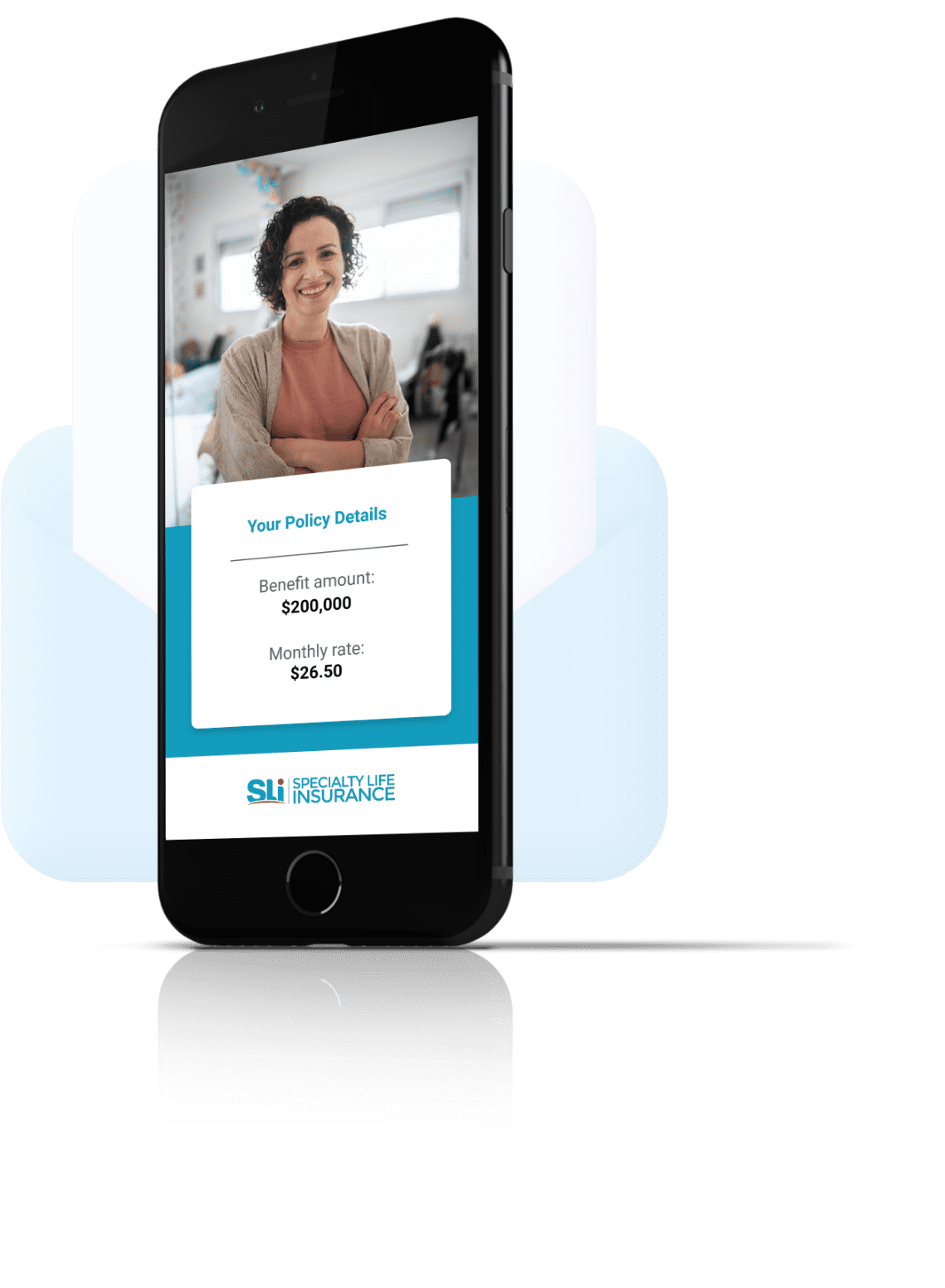

Secure coverage from $10,000 to $500,000 with no medical exams, bloodwork, or doctor’s reports. With a quick and easy application process, you can qualify and receive your policy the same day! Plus, Canadians with pre-existing conditions are eligible and welcome to apply.

Cancer Protection Add-On

Our optional cancer add-on can ensure you are protected up to $50,000 in case of a cancer diagnosis. This benefit helps ease financial worries, allowing you to focus on recovery.

Locked-In Premiums

Guaranteed fixed premiums – there are no surprises down the road, your premiums are guaranteed to stay level.

Flexibility

Choice of coverage duration for 10 or 20 years and an option to reduce your coverage amount, adjusting it to your changing needs. Your plan can be renewed or converted to a permanent policy without any additional health questions or medical exams.

Paramount Term Life Insurance is offered exclusively through Specialty Life Insurance and is underwritten by Humania Assurance.

What Our Clients Say

What is Term Life?

Term life insurance provides coverage for a selected period, such as 10, 20, or 30 years. In the event of your passing during this term, your designated beneficiary receives a tax-free payout.

Why do I need it?

If your family depends on your income, a life insurance payout can help cover daily expenses such as bills, groceries, and more, ensuring your loved ones can keep their quality of life.

A mortgage is usually the biggest financial obligation for a family. Life insurance acts as a safety net, providing peace of mind that your loved ones can keep their home, no matter what happens.

If you have a large amount of debt, a life insurance payout can ensure this financial burden doesn't fall on your family if you pass away.

Most parents agree that post-secondary education can help your children achieve their full potential. A life insurance benefit can ensure your children are able to get the foundation they need if you are no longer there.

Not sure if Term Life Insurance is the right choice?

Talk to our friendly licensed advisors today for a free, no pressure consultation.

SPEAK WITH A SPECIALISTApplying is a Breeze: Just Count 1-2-3

-

Apply Online

Apply for a quote on our website in under a minute!

-

Connect with Compassion

Connect with our licensed advisor, who will tailor your plan by discussing your needs, budget, and ask a few essential health questions. Receive a competitive quote along with a customized coverage recommendation just for you!

-

Seal the Deal with Ease

If everything looks good to you, let’s wrap it up! Complete the application process effortlessly over the phone. Soon after, your policy will be emailed to you, and it can also be mailed upon request. Voilà, you’re covered!

How much term life coverage do I need?

When thinking about how much coverage to apply for, there are several factors to consider, such as current financial obligations, future expenses, and more. Visit our Resource Centre for more information, including our CALCULATOR tool.

Visit Resource Centre

Top questions Canadians ask about Term Life Insurance

What is term life insurance and how does it differ from other types of life insurance?

Term life insurance provides coverage for a specified period or "term," offering a payout to the beneficiary if the insured passes away during that term. As compared to permanent types of life insurance such as Whole Life or Universal Life, Term Life Insurance is the most affordable option as it offers temporary protection and does not have an investment or cash value components.

Can I change my coverage after my policy is in force?

You can decrease the coverage amount as your needs change. However, there is no option to increase coverage.

Do my premiums change over time?

Your premiums remain fixed throughout the duration of your term and are guaranteed not to increase.

How much term life insurance do I need?

To determine how much term life insurance you need, consider your financial obligations, such as debts, future expenses like college tuition, and the income your family would need if you were no longer around. Our CALCULATOR is a handy tool to estimate the required coverage.

How long should my term (duration of coverage) be?

The length of term life insurance should align with your financial obligations and milestones, such as paying off a mortgage, your children completing secondary education, or your planned retirement age. Common term lengths are 10, 20, or 30 years, but you should choose a duration that provides coverage during the most financially vulnerable times for your dependents.

What factors affect my term life insurance premium?

Here are the factors that are taken into account when calculating your premiums:

Age: As age increases, so does the potential risk for insurers, leading to higher coverage costs.

Gender: Since women generally have a longer lifespan than men, men often face higher life insurance premiums.

Coverage Amount: Higher coverage levels result in an increased premium rate.

Smoking: Insurance rates for smokers can be double or more than those for non-smokers.

Health: Premiums increase with declining health, especially if you have conditions such as diabetes or high blood pressure.

Lifestyle considerations: Engaging in high-risk activities or occupations can result in elevated insurance rates.

What happens at the end of the term?

There are 3 options at the end of the term:

- Let your policy expire

- Renew your policy for another term

- Convert your plan into a permanent policy

With options 2 and 3 there is no need for additional health questionnaires or medical exams; however, your rates will be adjusted based on your current age.

Do I get my premiums back at the end of the policy or if I cancel my plan?

The premiums are not refundable at the end of the term.

If you cancel your policy within the 10-day review period, your premiums are refunded, after this review period the premiums are not refundable.

Is term life insurance benefit taxable and are premiums tax deductible?

In Canada, the life insurance benefit is not subject to taxation. In most cases your insurance premiums are not tax deductible, but speak to your accountant about any exceptions.

What are the common exclusions in a term life insurance policy?

The most coming exclusion is the suicide clause. It states that the no death benefit will be paid if the insured commits suicide within two (2) years of the effective date of coverage.